Delving into Fixed-Rate Mortgages in Germany: Why 10-Year and 15-Year Terms Are the Safest Bet, this introduction immerses readers in a unique and compelling narrative, with casual formal language style that is both engaging and thought-provoking from the very first sentence.

Fixed-rate mortgages provide stability and predictability to borrowers, offering a secure financial option. In this article, we will explore why 10-year and 15-year terms are considered the safest bet in Germany's mortgage market, balancing affordability with long-term planning.

Overview of Fixed-Rate Mortgages in Germany

Fixed-rate mortgages in Germany are a popular choice among borrowers due to their stable and predictable nature. These mortgages have an interest rate that remains constant throughout the entire term of the loan, providing borrowers with the security of knowing exactly how much they need to pay each month. This stability and predictability make fixed-rate mortgages a safe bet for many homeowners.

Fixed-rate mortgages in Germany are a popular choice among borrowers due to their stable and predictable nature. These mortgages have an interest rate that remains constant throughout the entire term of the loan, providing borrowers with the security of knowing exactly how much they need to pay each month. This stability and predictability make fixed-rate mortgages a safe bet for many homeowners.Stability and Predictability

Fixed-rate mortgages offer borrowers the peace of mind of knowing that their monthly mortgage payments will not change, regardless of any fluctuations in the market interest rates. This stability makes budgeting easier and helps borrowers avoid any surprises in their monthly expenses. Additionally, fixed-rate mortgages provide protection against rising interest rates, as borrowers lock in a rate at the beginning of the loan term.Comparison with Other Loan Types

In contrast to fixed-rate mortgages, adjustable-rate mortgages (ARMs) have interest rates that can change periodically based on market conditions. While ARMs may initially offer lower interest rates, they come with the risk of interest rate hikes in the future, leading to potentially higher monthly payments for borrowers. On the other hand, fixed-rate mortgages ensure that borrowers have a consistent monthly payment amount for the entire duration of the loan, providing financial security and peace of mind.Importance of 10-Year and 15-Year Terms

When it comes to fixed-rate mortgages in Germany, the choice between a 10-year and 15-year term is crucial for borrowers looking for stability and security in their financing options. These terms are popular choices for several reasons, offering a balance between affordability and long-term planning.

Reasons for Popularity

Both 10-year and 15-year terms are favored by borrowers due to their predictability and stability. With fixed monthly payments throughout the term, borrowers can easily budget and plan for their future expenses. Additionally, these terms provide protection against rising interest rates, giving borrowers peace of mind knowing that their mortgage payments will remain constant.

Affordability and Long-Term Planning

- 10-Year Terms: Shorter terms like the 10-year option often come with lower interest rates compared to longer terms, making them attractive for borrowers seeking to pay off their mortgage sooner and save on interest costs. While monthly payments may be higher, the overall interest paid over the term is significantly lower.

- 15-Year Terms: On the other hand, 15-year terms strike a balance between affordability and quicker equity building. Borrowers benefit from a slightly longer term with lower monthly payments compared to a 10-year term, allowing for more flexibility in budgeting while still aiming to pay off the mortgage faster.

Benefits of Short-Term vs. Long-Term Fixed-Rate Mortgages

Short-term fixed-rate mortgages like the 10-year term offer the advantage of lower interest rates, reduced overall interest costs, and faster repayment. On the other hand, long-term fixed-rate mortgages such as the 15-year term provide a balance between manageable monthly payments and accelerated equity building, giving borrowers more financial security and stability over a slightly longer period.

Safety and Security of Fixed-Rate Mortgages

Fixed-rate mortgages offer borrowers a level of safety and security by protecting them from interest rate fluctuations. With a fixed rate, borrowers have the peace of mind of knowing that their monthly payments will remain consistent throughout the term of the loan, regardless of how market interest rates may changeFinancial Security with Fixed-Rate Mortgages

- One scenario where fixed-rate mortgages provide financial security is during periods of rising interest rates. Borrowers with fixed-rate mortgages are shielded from the impact of increasing rates, as their mortgage payments remain unchanged.

- Another example is the predictability of budgeting with fixed-rate mortgages. Borrowers can easily plan their finances without worrying about unexpected spikes in mortgage payments due to interest rate hikes.

- Fixed-rate mortgages also offer protection against economic uncertainty. In times of economic instability, having a fixed mortgage rate ensures that borrowers can maintain their housing costs without being affected by external financial factors.

Why Fixed-Rate Mortgages are Considered Safe

Fixed-rate mortgages are considered a safe bet for many borrowers because they eliminate the risk of payment shock from interest rate increases, providing stability and predictability in housing expenses.

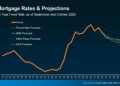

Market Trends and Interest Rates in Germany

In the dynamic landscape of the real estate market in Germany, market trends and interest rates play a crucial role in shaping the preferences of borrowers when it comes to choosing different mortgage terms.Impact of Market Trends on Mortgage Term Popularity

- Market trends such as economic stability, housing demand, and inflation rates can influence the popularity of different mortgage terms.

- During periods of economic uncertainty, borrowers may prefer longer mortgage terms like 10-year or 15-year fixed-rate mortgages for stability and predictability in payments.

- Conversely, in times of economic growth and low-interest rates, shorter mortgage terms may become more popular due to lower overall interest costs.

Current Interest Rate Environment in Germany

- The interest rate environment in Germany is currently characterized by historically low rates, making fixed-rate mortgages an attractive option for borrowers.

- Low interest rates provide borrowers with the opportunity to lock in favorable rates for an extended period, offering protection against potential rate hikes in the future.

- Fixed-rate mortgages, especially 10-year and 15-year terms, are popular choices in Germany due to the stability they offer amidst fluctuating market conditions.

Economic Factors and Borrower Decision-Making

- Economic factors such as employment rates, GDP growth, and consumer confidence can impact the decision-making process for borrowers when selecting a mortgage term.

- Borrowers often consider the overall economic outlook and their own financial stability when choosing between different mortgage terms, weighing the benefits of short-term savings versus long-term security.

- The predictability and security of fixed-rate mortgages, coupled with the prevailing economic conditions, guide borrowers towards 10-year and 15-year terms as the safest bet in the German market.

Last Word

In conclusion, opting for a fixed-rate mortgage in Germany, particularly with 10-year or 15-year terms, provides a secure and reliable financial choice for many borrowers. The stability they offer in an uncertain market makes them a popular and safe option for those looking to invest in property.

Expert Answers

Are fixed-rate mortgages the most secure option for borrowers in Germany?

Yes, fixed-rate mortgages in Germany provide protection from interest rate fluctuations, offering stability and security to borrowers.

What are the advantages of choosing a 10-year or 15-year fixed-rate term?

These terms strike a balance between affordability and long-term planning, giving borrowers a sense of security while ensuring manageable payments.

How do economic factors influence the decision-making process for borrowers when it comes to fixed-rate mortgages?

Economic conditions such as interest rates and market trends play a significant role in borrowers' choices, impacting the popularity of different mortgage terms.

{kind=link}