Embark on a comprehensive journey through the realm of VA Home Loans in 2026, exploring eligibility requirements, interest rates, and hidden benefits. This guide is designed to provide a detailed insight into the world of VA Home Loans, offering valuable information and guidance to potential borrowers.

Overview of VA Home Loans

VA Home Loans are mortgage loans available to eligible veterans, service members, and their families, guaranteed by the U.S. Department of Veterans Affairs. They are designed to help make homeownership more accessible for those who have served in the military.

Brief History of VA Home Loans

VA Home Loans were established in 1944 through the Servicemen's Readjustment Act, also known as the GI Bill. The program was created to provide veterans with a pathway to homeownership as a way to thank them for their service. Over the years, VA Home Loans have evolved to offer more flexible terms and benefits to better serve military borrowers.

Key Features of VA Home Loans

- Zero Down Payment: One of the most significant benefits of VA Home Loans is the ability to purchase a home with no down payment, making it easier for veterans to become homeowners.

- No Private Mortgage Insurance (PMI): VA Home Loans do not require PMI, which can save borrowers hundreds of dollars each month compared to conventional loans.

- Competitive Interest Rates: VA Home Loans often offer lower interest rates compared to conventional mortgages, saving borrowers money over the life of the loan.

- Flexible Credit Requirements: VA Home Loans have more lenient credit score requirements, making it easier for veterans with less-than-perfect credit to qualify for a loan.

- No Prepayment Penalties: Borrowers can pay off their VA Home Loan early without facing any prepayment penalties, allowing them to save on interest costs.

Eligibility Criteria

When considering a VA Home Loan in 2026, it is crucial to understand the eligibility criteria that determine who can qualify for this type of mortgage.

Service Requirements

- Active-duty service members, veterans, National Guard and Reserve members, and certain surviving spouses may be eligible for a VA Home Loan.

- Minimum service requirements vary depending on the time period served, ranging from 90 consecutive days during wartime to 181 days during peacetime.

- Recent changes in service requirements have expanded eligibility to include more categories of service members and veterans, making it easier for individuals to qualify for a VA Home Loan.

Credit Score

- While the VA does not set a minimum credit score requirement, most lenders prefer a score of at least 620 for VA Home Loan approval.

- Borrowers with lower credit scores may still be eligible, but they might encounter higher interest rates or additional requirements.

- In 2026, the credit score requirements for VA Home Loans have remained relatively stable compared to previous years, with lenders focusing more on the overall credit profile of the borrower.

Income Criteria

- Borrowers must have a stable income that is sufficient to cover their monthly mortgage payments, living expenses, and other debts.

- The debt-to-income ratio is a crucial factor in determining eligibility, with most lenders looking for a ratio below 41%.

- Recent changes in income criteria have included adjustments to the way certain types of income are calculated, impacting how lenders assess a borrower's ability to repay a VA Home Loan.

Interest Rates and Financing Options

When it comes to VA Home Loans, understanding the interest rates and financing options available is crucial in making informed decisions about your home purchase.

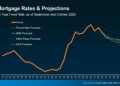

Current Interest Rates for VA Home Loans

As of 2026, VA Home Loans typically offer lower interest rates compared to conventional mortgage rates. These rates are determined by various factors such as the borrower's credit score, loan term, and market conditions. It is essential to stay updated on the latest interest rates to ensure you get the best deal on your VA Home Loan.

Financing Options for VA Home Loans

There are different financing options available for VA Home Loans to suit the needs of borrowers. Two common options are fixed-rate mortgages and adjustable-rate mortgages.

- Fixed-Rate Mortgages: With a fixed-rate mortgage, the interest rate remains the same throughout the loan term. This provides predictability in monthly payments and protection against interest rate hikes.

- Adjustable-Rate Mortgages: An adjustable-rate mortgage has an interest rate that can fluctuate based on market conditions. While initial rates may be lower, they can increase over time, potentially affecting your monthly payments.

Impact of Interest Rates on the Overall Cost

Interest rates play a significant role in determining the overall cost of a VA Home Loan over time. Even a small difference in interest rates can result in substantial savings or additional costs throughout the loan term. It is essential to consider how interest rates can impact your financial situation and choose the financing option that aligns with your long-term goals.

Hidden Benefits and Cost Savings

When it comes to VA Home Loans, there are several hidden benefits and cost-saving advantages that borrowers should be aware of. These perks can make a significant difference in the long-term financial health of those utilizing VA loans.

No Down Payment Requirement and No PMI

One of the most notable benefits of VA Home Loans is the fact that they do not require a down payment. This can save borrowers thousands of dollars upfront, making homeownership more accessible. Additionally, VA loans do not require private mortgage insurance (PMI), which is typically a requirement for conventional loans with a down payment of less than 20%.

Lower Closing Costs and Interest Rate Discounts

Another cost-saving advantage of VA Home Loans is the potential for lower closing costs compared to traditional mortgages. VA loans limit the amount borrowers can be charged for closing costs, helping to reduce the financial burden of buying a home. Additionally, many lenders offer interest rate discounts to veterans and active-duty service members, further reducing the overall cost of borrowing.

Examples of Cost Savings

- For example, a borrower purchasing a $250,000 home with a traditional loan requiring a 20% down payment would need to pay $50,000 upfront. With a VA loan, that same borrower could purchase the home with no down payment, saving a significant amount of money at the outset.

- In another scenario, a veteran refinancing their home with a VA loan could benefit from lower closing costs and interest rate discounts, resulting in substantial long-term savings on their mortgage payments.

Conclusion

In conclusion, The Complete Guide to VA Home Loans in 2026 sheds light on the intricacies of securing a VA Home Loan, highlighting the benefits, eligibility criteria, and financial implications. Whether you're a military service member or a curious reader, this guide equips you with the knowledge needed to navigate the world of VA Home Loans with confidence.

Top FAQs

What are the service requirements for VA Home Loans?

To be eligible for a VA Home Loan, individuals must meet specific service requirements based on their military status and length of service.

Are there any recent changes in eligibility criteria for VA Home Loans?

As of 2026, there have been no significant changes in the eligibility criteria for VA Home Loans compared to previous years.

How do interest rates impact the overall cost of a VA Home Loan?

Interest rates play a crucial role in determining the total cost of a VA Home Loan over its term. Borrowers should consider the impact of interest rates on their monthly payments and long-term financial commitments.

What are the hidden benefits of VA Home Loans?

VA Home Loans offer advantages such as no down payment requirement, no private mortgage insurance, and potential cost savings in terms of closing costs and interest rate discounts.